I first wrote about the All-Weather Portfolio a year or two back on Financial Horse.

It’s quite a popular one, and I frequently get questions on it – I guess there’s just something about a portfolio that does well in all economic conditions that appeals to us, especially in these volatile times.

Quite a lot of things have changed since, so I wanted to revisit the topic, and adapt the All-Weather Portfolio for 2020, for Singaporeans.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything. Sign up below (you get a free guide when you sign up):

Basics: All Weather Portfolio

The All Weather Portfolio has its roots in Modern Portfolio Theory.

I won’t go into it in detail, but the essence has to do with exploiting correlations between asset classes.

For example, when stocks prices go down, US Treasuries go up, and vice versa, so if you mix stocks with Treasuries, you have far less volatility in your portfolio, and the risk adjusted returns go up. That’s the crux of the 60/40 portfolio btw.

Anyway the more asset classes you add (eg. Gold, commodities etc), the more you reduce volatility, and the higher the risk adjusted returns.

So there’s no such thing as a free lunch in investing, but diversification really is a free lunch. It increases your risk adjusted returns at little to no cost to you.

So diversification is just a complete no brainer.

It’s one of the topics we go in depth into in the REITs Masterclass if you’re interested to learn more.

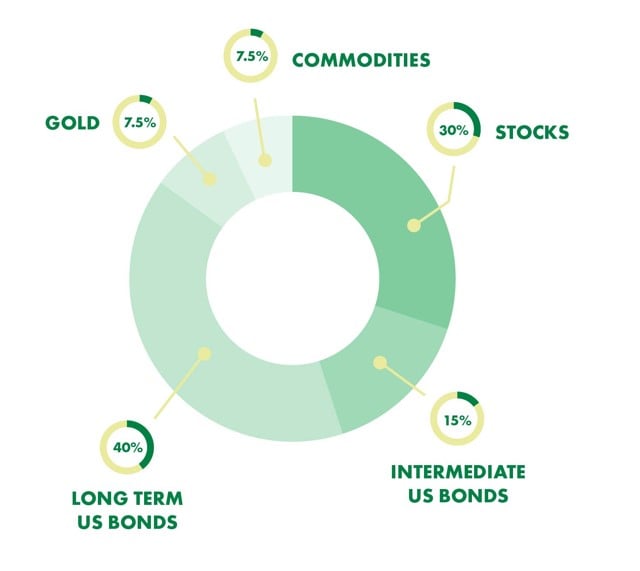

Anyway, the original All Weather Portfolio was proposed by Ray Dalio for US Investors, and it looks like this:

For the 30 year period from 1984 to 2013, this portfolio returned 9.7% annual returns, against 7.2% annual returns for a 35/65 stock/bond portfolio (47% in long-term treasuries, 18% in 10 year treasuries and 35% in the S&P 500).

Problems with the All Weather for Singaporeans

Fast forward to 2020, and the All Weather portfolio doesn’t work so well anymore, especially for Singaporeans. There are a few key problems with the All Weather for Singaporeans:

Long term treasuries no longer have capital gains

The single biggest problem with the All Weather is that US interest rates are now zero bound.

The key of the All Weather lies in the long term US Treasury component – it assumes that as stocks drops, long term US Treasuries will go up. That’s why 40% of the portfolio goes into long term US Treasuries.

What happens now is that when US interest rates hit the zero bound, that assumption no longer holds true.

The logic goes like this right. Bond prices go up with yields fall. So if you’re holding a US Treasury, you make money when the yields fall. And over the past 30 years, yields have fallen from 15% to 0%, which is why long dated US Treasuries are one of the best investments ever in this 30 year period, outperforming even stocks.

The problem now – the 10 year Treasury now sits at 0.73% yield, and the 30 year sits at 1.5%.

Sure, they can still go down and hit 0%, but what happens after that?

Now there’s some debate about whether the Feds will eventually have to go into negative rates. My personal view is that they won’t, but I can’t rule out that possibility as well.

But even if we accept that possibility, and we assume rates can go to -1%, that just extends the life of the US Treasury by a few years.

At some point in the future, capital gains on US Treasuries will cap out, simply because interest rates cannot drop anymore.

It doesn’t matter if you’re investing for a 2 to 3 year period, but if you plan to build an All Weather to last the next 10 to 20 years, that’s something you’ll really need to think about.

Because once US Treasuries no longer have capital gains, the negative correlation with stocks drops, and US Treasuries become no more than glorified cash.

This in itself, would destroy a fundamental pillar on which the entire All Weather Portfolio rests. Almost 55% of the All Weather Portfolio goes into Treasuries, and there’s just no replacement for this asset class in the world.

USD exposure is not ideal long term

The next problem here is that the USD exposure is not ideal for Singapore investors in the longer term. It makes sense if you’re an Emerging Market like Turkey or Brazil (to hold lots of USD).

But in Singapore, where the country is generally well managed, and the SGD appreciates against the USD over time, you don’t necessarily want to have 55% of your portfolio exposed to USD.

So that’s a problem as well.

Singaporeans love Real Estate (and we have CPF)

Now the All Weather Portfolio is designed for Americans right. Who apparently spend all their money, have little savings, and don’t own their property (if you trust the popular media).

Contrast that with a Singaporean who saves a lot, and loves to invest in property. And has mandatory CPF.

So the problem with the All Weather Portfolio from Ray Dalio?

It doesn’t provide for (1) Singaporean’s kiasu, property grabbing nature, and (2) CPF.

Both of which are big for Singaporeans, so the All Weather is definitely not perfect for us.

All Weather Portfolio for Singaporeans

So let’s make some tweaks to the All Weather Portfolio, to refresh it for 2020, and to adapt it for Singaporean Investors.

Here’s my proposed mix:

- Gold – 10%

- Commodities – 5%

- Fixed Deposit / SSBs (Short Term) – 15%

- CPF OA / SA – 20%

- Stocks / REITs – 20%

- Real Estate – 30%

For obvious reasons, this formula shouldn’t be set in stone.

I’ll explain my thinking for each component, and once you understand the rationale, you can adapt it for your own situation accordingly.

Gold – 10%

I love gold – as a hedge.

Every investor needs that one asset class that can stay separate from the financial markets, and that will retain its value (or even better, appreciate in value) when shit hits the fan.

With US rates at zero bound, US Treasuries are somewhat less effective at that role longer term, so gold looks more and more attractive.

The mistake most investors make with gold is to think of it as an investment. It’s not.

In a balanced portfolio, gold is a hedge, So in the good times, gold does nothing, and it may drop in price, but the rest of your portfolio, the stocks, REITs and real estate, those will go up in prices. Because when gold goes up big time, the rest of the portfolio will suffer.

So think of gold as the price of insurance. When you’re paying the price of insurance, it means everything else is going fine. But when the insurance is paying you, you’ll be glad you bought it.

So ask yourself – would you rather be paying insurance, or would you rather the insurance pay you?

Commodities – 5%

I know it looks stupid to include commodities when we’re in a 10 to 20 year bear market for commodities.

Commodities have been completely crushed over the past 10 to 20 years, but I think that in some point going forward, the world is going to flip from a deflationary regime into an inflationary regime.

All that QE and money printing over the past 10 years actually contributed to a slower growth environment that was horrible for commodities. But going forward, I believe that switches, and we may start the transition into an inflationary scenario.

The problem? The timing is close to impossible to predict. But the beauty with an All Weather – you don’t have to get the timing right, you just need to own it.

There are many ways to play this, and instead of owning the underlying commodity (which has roll costs), one other way is to own commodity producers, and let them do the dirty work of monetizing commodities. Do watch the creditworthiness of the companies though.

Fixed Deposit / SSBs (Short Term) – 15%

The idea here is the same as that in the All Weather. We need to have some cash on hand, that generates good returns, but isn’t subject to big volatility. This is our emergency buffer if you like.

It doesn’t make sense to hold our emergency buffer in USD, so we’ve completely switched it over to SGD.

You know the drill here – put it where ever it can earn you the highest returns, with close to zero risk.

So use DBS Multiplier, UOB One, StashAway Simple (money market fund), fixed deposits, Singapore Savings Bonds, whatever floats your boat.

CPF OA / SA – 20%

So how do you get around the problem that US Treasuries may no longer have capital gains going forward?

And I think the simple answer is that there is no solution to that. There is no asset class in this world that can replace exactly the function that US Treasuries used to have in the All Weather.

The only workable solution I have so far is to (1) accept that US Treasuries are now glorified cash, (2) accept higher volatility in the portfolio going forward, and (3) beef up on protection in other ways.

For Singaporeans, CPF contribution is mandatory anyway, so we might as well just make use of it.

It’s risk free, generates a decent return, and if you leave it in CPF-OA it can even be used to pay your mortgage or invest.

This opens up a lot of possibility to balance between CPF-OA and CPF-SA based on the stage of your life you are in.

If you are young, you might want to keep more in CPF-OA to fund your house. If you are older and have settled your house, you might want to keep more in CPF-SA.

If you’re a sophisticated investor, you can even put some in US Treasuries, because short term, I think there is still some potential for capital gains. This will probably go once the Feds implement yield curve control though.

Real Estate (Private Real Estate in Singapore) – 30%

So everything above, is mainly just protection, and diversification. And that’s a whopping 50% of the portfolio.

Everything else from here on out, is for investment gains.

To put it in footballing terms, everything above is the defence and defensive midfield. It’s there to protect you. But you don’t win the game by playing defence. You win the game by scoring goals.

So Real Estate and Stocks / REITs? These are the strikers and attacking midfield. They are here to grow your net worth.

To be honest, this 50% can be split between real estate, stocks and REITs, depending on your personal preferences, and the stage of your life.

Some people don’t like the volatility that comes with capital markets, in which case real estate could be a better bet. In Singapore, the private residential market is pretty controlled by the regulatory authorities, so you won’t have the wild swings in prices that you get with stocks.

That’s both good and bad, depending on the kind of investor you are.

The problem with real estate ultimately, is that you just won’t get the same kind of returns that you saw the past 50 years. Over the last 50 years, Singapore went from backwater port to first world status, and property prices have exploded accordingly. But that’s a once off, and it won’t happen again. Going forward, I probably expect low single digit gains for real estate on average in Singapore.

But because Real Estate throws on so much leverage, that low single digit gains could still turn out well based on the amount you’re putting in, because you’re basically juicing it up with leverage.

Stocks / REITs – 20%

Finally, we have stocks and REITs.

It’s been reduced from the 30% in the original All Weather, because I wanted to buffer more in for real estate. This is Singapore after all, and most of us probably have more money in real estate than in stocks.

And within this 20%, is really what the entirety of Financial Horse is about, so check out any of the other articles on this site for ideas on how to invest.

Some people like to buy a passive index, some people like to active invest.

For me, I like to split it between US, China, and Singapore, and I like to split it between growth and yield plays.

My personal stock watchlist is available on Patron if you’re keen.

Closing Thoughts: There’s no one size fits all

And I think the key lesson here is that there’s really no one size fits all portfolio. Everybody’s portfolio is unique, because everybody’s financial situation is unique. Some people like to have an extra investment property rather than more stocks. Some people have an iron ricebowl job so they can reduce their cash position. Some people have high earnings power but poor job security, so they need to hold more cash.

Your portfolio, should reflect your financial situation, and your own character.

For me personally, I’ve found what works for me, and I’m happy with it so far. My entire personal portfolio is available on Patron for those who are keen, which is based loosely on some of the principles set out here.

I practice a bit more active investing, so while I use the All Weather as the base, I make tactical adjustments based on the stage of the economic regime that we are currently in. For example, if I believe we are late stage in the debt cycle, I may dial back on stocks and hold more cash. If I believe we are transitioning into inflation, I would hold more stocks and real estate, and less cash / bonds.

Even if you don’t like All Weather style portfolios, it’s important to understand the logic that goes into them. Once you understand the logic, you can then tailor it to suit your own investment objectives.

As I always say on Financial Horse, it’s actually asset allocation that determines the bulk of your returns, not stock picking. Go for the 80/20 rule here. Never neglect asset allocation.

I would really love to hear your comments though. How do you guys invest your own portfolios? Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Dear Financial horse.

Good article as always. 2 of my thought are as follows:

1) as you correctly pointer out that the allocation % differs from individual specific situation. Iron rice bowl type vs property agent etc. fresh graduate vs those with over 20 years of work experience etc. if you like, maybe you can consider proposing a few different Allocation proportions for folks from different age group to guide everyone closer?

2) notice that in this model, there are 6 categories. A typical SG person will have a big chunk of their total fund are lock up in CPF as well as the real asset (flat/condo). The left over available cash might be too little to spread over the remaining 4 categories to have meaning effect. ( not forgetting it is a good practise to set aside emergency fund that is usual is worth about 6 month of monthly expense can be park into accounts like DBS multiples account will further zap away more of the free fund). Maybe can consider to shrink from 6 categories to 4 categories. Doing so definitely will make this model less all weather but might more easy to apply.

For your comment please.

Thanks for sharing! My thoughts:

1) Yes! We have done exactly this under the FH Course: https://financialhorsecourse.thinkific.com/courses/complete-guide-to-investing-for-singapore-investors

2) Doing so will drop the effectiveness of the portfolio though. If I really had to, I would drop commodities and allocate that amount to gold. But the rest needs to stay. It’s not all that hard to keep it up, because some like CPF/Cash are pretty automated, so that’s already 2 asset classes that you don’t need to think about.

Hi FH, you gave gold a 2 out of 5 Financial Horse rating previously in 2018. Now that you mentioned loving gold as a hedge during such volatile times, does it mean that its rating has gone up?

I think gold didn’t make sense in the post QE1 era (approx 2012 onwards). But after the market plunge in late 2018, and the Feds changing their mind about rate cuts (started cutting rates), I think gold suddenly regained its relevance. Especially as we approach the end stage of this long term debt cycle.

Hi I would like to know what type of gold should I consider? never bought before , but right now, im looking hard into GOLD ETFS as a hedge, as im holding to quite a number of local stocks. Can I kindly know whats your view on gold etfs ?

As long as the gold ETF is backed by physical gold, should be fine. Physical gold works too, but higher transaction costs.

Gold miners are good if you want a leveraged play on gold.

Hi FH, It’s not clear to me why USD exposure is not ideal for singapore investors in the long term. Could you elaborate?

Well it really depends on your view on the USD. Over the past 10 to 20 years, USD has generally weakened against the SGD, and I do expect that to hold up to a certain extent going forward. So some USD exposure is okay, but too much is not ideal too. It’s about finding that right balance for your own risk appetite.

Love this as usual. Particularly how gold is like insurance. Can you share bit more on gold? Ie. are you buying physical, or mining shares or?

I would say go with physical or ETF (physical backed) to be on the safe side, go with mining shares if you want something with more leverage. I’ll see if I can do a post on gold. 🙂

Hi FH,

Great article as usual. I found your thoughts on role of US treasuries particularly thought provoking.

A few comments

1. While vanilla US treasuries face the challenges you mention, what do you think about US TIPS? While gold is an inflation hedge, they don’t pay you while you wait and are subject to quite large fluctuations. US TIPS will payoff if indeed inflation rears its head again and are potentially less volatile. True that there is still a currency risk and so this will have to be taken into account into proportion of portfolio it makes up.

2. I am not sure about the high 30% allocation to real estate. Is this investment real estate or real estate for own stay? As you know, latter does not provide any yield and so you are dependent on capital appreciation.

Regardless of whether for own stay or investment, I think there is a real risk of a bubble here, especially in the next few years. Private real estate in Singapore is already the second most expensive in the world after Hong Kong and we all know the social unrest it caused there. So how much higher can it go without causing social issues? Not much probably given the widespread unhappiness during the 2011 GE. Buying into it at this point would mean buying into something that is already priced among the highest in the world, not something one would typically do in any asset class. Furthermore, in 2022/23, we will see a slew of developments facing ABSD charges and it is likely that the effects of the Covid crisis are still being felt then, even if recovery starts in 2021. So you could have the perfect storm of overpriced developments facing ABSD and a weak economic environment at the same time. I suspect there will be a lot of fire sales then by developers, we have already seen the first two.

Furthermore, if you have physical real estate and REITs as well in different categories, you will be a lot more invested in real estate overall than in equity. Is that the appropriate balance? Over time, it has been shown that equity returns have outperformed real estate in the US. True that in Singapore, real estate has outperformed the US S&P but as you say, that was a different era while we were moving from third world to first.

3. What would the overall return be on the portfolio you constructed? I recognize that in today’s world, everything is expensive and yields are low so it is hard to have decent returns no matter what one constructs.

4. Finally, back to a question I posed earlier, How do we adapt this to a $10M portfolio? The SSB/CPF portions will probably make up only ~10% of such a portfolio with no possibility of increasing allocation to them.

Thanks a lot for your thoughts!

Hi CMC,

Really good questions as usual. Really enjoyed them. My thoguhts:

1) Yes, I think TIPS are a good option as well, especially from a diversification perpective. Some gold + TIPS would be great protection against inflation. The tricky part is deciding on the right allocation to TIPS, which ultimately will have to go back to asset allocation and positioning.

2) I think the 30% allocation shouldn’t be set in stone. Think of it more like a 50% allocation to Stocks, REITs and Real Estate. The size of the real estate component will depend on the individual in question. Younger investors will have a bigger %, older ones less. Not every likes real estate, so for those, the money can be allocated into REITs or Stocks.

3) I actually disagree on private real estate being in a bubble. I think the Govt has been very careful to control demand / supply, and the cooling measures have gone a long way in preventing the blow off top in real estate prices. Without a blow off top, there’s no real bubble / over exuberance, so conversely there is no big crash as well. That said, I do agree that we will probably see a moderation in real estate prices, perhaps in the 5% to 10% range? But personally, don’t see this playing out as a 1997 AFC style fire sales, but happy to be proven wrong.

4) On a historical basis, returns would have been great, 6 to 8% range. But nobody cares about historical return, we care more about future returns. And I think that with the risk free rate so close to 0%, one definitely has to temper expectations as to returns. Can’t achieve the same returns as in the past without taking on more risk.

5) The key difference for a $10m portfolio is where to park the cash. SSBs/CPF won’t work, so I’d prob go with a combination of fixed deposit or money market funds. Singapore Government bond funds could be good also, but horrible liquidity with those.

Hope this helps! Great thoughts from you as always.

Hi FH,

Would you mind doing a post on IFast? Got strong prospect & Sentiments for this counter for the upcoming years.